Starting from January 2018, the non-financial reporting Directive (2014/95/EU) has made large public interest entities with over 500 employees (listed companies, banks, and insurance companies) obliged to disclose the non-financial information. As required by the directive, the Commission has published non-binding Guidelines in 2017 to help companies disclose relevant non-financial information in a more consistent and more comparable manner. Yet, in June 2019, the Commission has issued guidelines on reporting climate-related information which provide companies with practical recommendations on how to better report the impact of their activities on climate, as well as the impact of climate change on their business.

The new Guidelines on climate-related disclosures

The EU is dedicated to reducing greenhouse gas (GHG) emissions and creating a low-carbon and climate-resilient economy. In the EU’s quest for a prosperous, modern, competitive and climate-neutral economy by 2050, companies and financial institutions will have a critical role and thus, the Commission appointed the Technical expert group on sustainable finance (TEG) to provide guidance on climate reporting as part of the Sustainable Finance Action Plan, adopted in March 2018. The aim of the Sustainable Finance Action Plan is ‘’reorienting capital towards sustainable investment, managing financial risks that arise from climate change and other environmental and social problems and fostering transparency and long-termism in financial and economic activity’’. According to the Guidelines, “corporate disclosure of climate-related information has improved in recent years. However, there are still significant gaps, and further improvements in the quantity, quality and comparability of disclosures are urgently required to meet the needs of investors and other stakeholders” and ‘‘without sufficient, reliable and comparable sustainability-related information from investee companies, the financial sector cannot efficiently direct capital to investments that drive solutions to the sustainability crises’’. It is important to note that the new Guidelines integrate the TCFD recommendations established by the G20’s Financial Stability Board.

Benefits for reporting companies

Better disclosure of climate-related information can have numerous benefits for the reporting company itself, such as:

- increased awareness and understanding of climate-related risks and opportunities better risk management, and more informed decision-making and strategic planning;

- a more diverse investor base and a potentially lower cost of capital, resulting for example from inclusion in actively managed investment portfolios and in sustainability-focused indices, and from improved credit ratings for bond issuance and better credit worthiness assessments for bank loans;

- more constructive dialogue with stakeholders, in particular investors and shareholders;

- better corporate reputation and maintenance of social licence to operate.

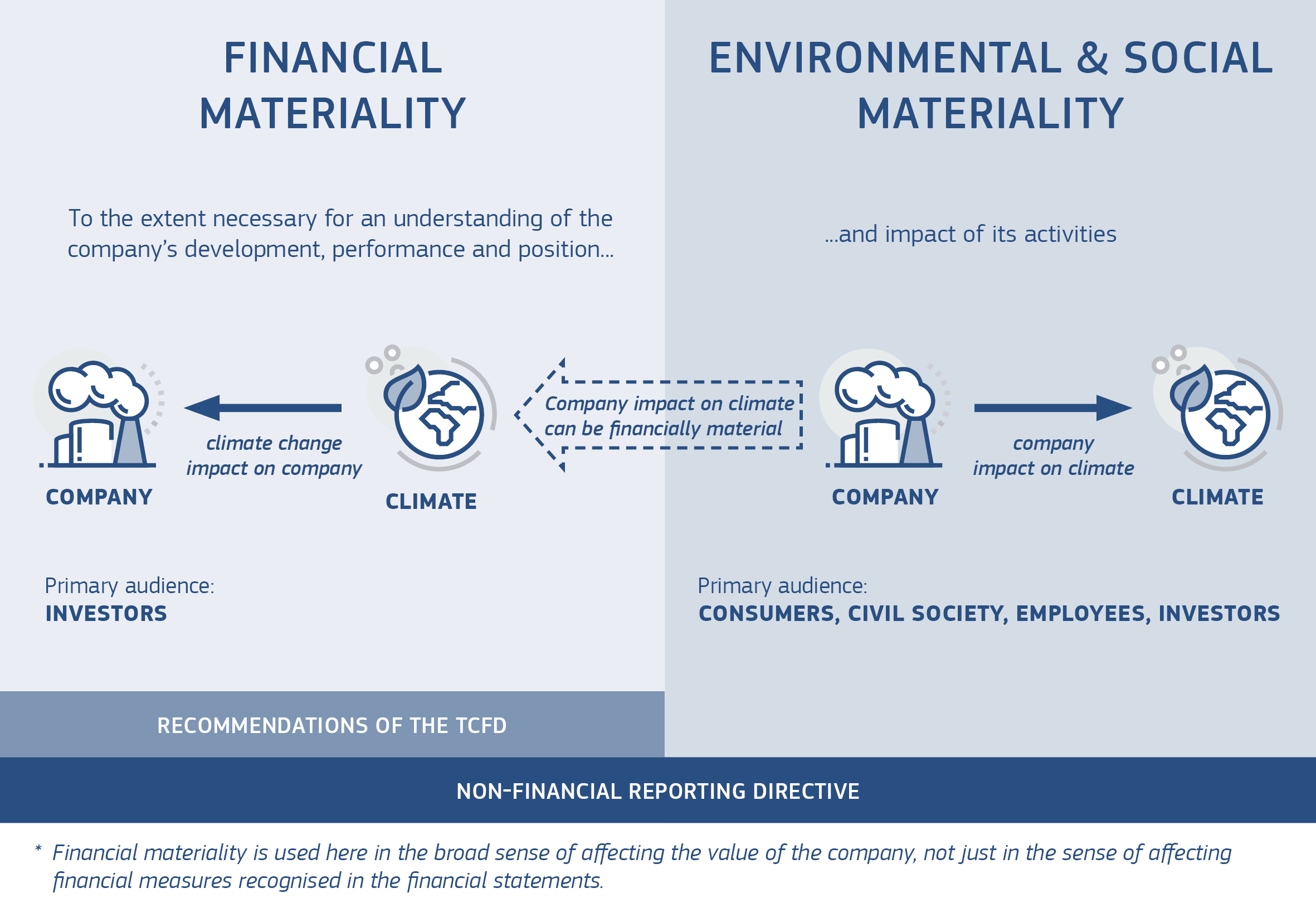

The double materiality perspective

Table 1: The double materiality perspective of the Non-Financial Reporting Directive in the context of reporting climate-related information (Source: https://eurlex.europa.eu/legalcontent/EN/TXT/PDF/?uri=CELEX:52019XC0620(01)&from=EN)

It is well-known that a company is required to disclose information on environmental, social and governance issues, and climate-related information falls into the category of environmental matters. Yet, in the Commission’s new non-Binding Guidelines on Non-Financial Reporting, the reference to the “impact of [the companies’] activities” introduced a new element to be taken into account when assessing the materiality of non-financial information, revealing that the Non-Financial Reporting Directive has a double materiality perspective:

- The reference to the company’s “development, performance [and] position” indicates financial materiality, in the broad sense of affecting the value of the company. Climate-related information should be reported if it is necessary for an understanding of the development, performance and position of the company. This perspective is typically of most interest to investors.

- The reference to “impact of [the company’s] activities” indicates environmental and social materiality. Climate-related information should be reported if it is necessary for an understanding of the external impacts of the company. This perspective is typically of most interest to citizens, consumers, employees, business partners, communities and civil society organisations. However, an increasing number of investors also need to know about the climate impacts of investee companies in order to better understand and measure the climate impacts of their investment portfolios.

The materiality perspective of the non-Financial Reporting Directive covers financial materiality as well as environmental and social materiality.

As per the Guidelines, companies are advised to consider their whole value chain, both upstream and downstream, when assessing the materiality of climate-related information. Yet, companies that conclude that climate is not a material issue are advised to consider making a statement to that effect, explaining how that conclusion has been reached.

How companies should approach the new Guidelines?

Companies are advised to study the supplement together with the applicable national legislation transposing the Non-Financial Reporting Directive (2014/95/EU), and the text of the Directive itself. Companies, ‘‘should also consider the Non-Binding Guidelines on Non-Financial Reporting published by the Commission in June 2017 , which contain 6 key principles for good non-financial reporting” according to which, the “disclosed information should be: (1) material; (2) fair, balanced and understandable; (3) comprehensive but concise; (4) strategic and forward-looking; (5) stakeholder-oriented; and (6) consistent and coherent.’’. Moreover, companies are encouraged to read the recommendations of the TCFD, and if relevant the supplementary guidance for the financial sector and for companies operating in the sectors of energy, transport, material and buildings, and agriculture, food and forest products. When it comes to starting date, companies should be able to use the new Guidelines for reports published in 2020, covering financial year 2019. The Guidelines urge companies to look beyond compliance, and focus on new business models, impact driven disclosures to ensure they remain relevant, profitable and sustainable in this new low-carbon and climate-resilient economy.